So you are decided, you will go legit and to save on cost you decide to do it on your own (hmm sure ka baka magsisi ka pero sige). Naturally your first question would be:

You yourself must first ask this very important question.

Sole proprietorship or Corporation which will you choose?

We say that this is the most important question in business registration because your answer to this will greatly affect how you will go through the next steps of registration and of course the tax implications.-

To help you with this question we lay out differences between the two in the following aspects:

As to registration or regulatory body?

If you choose to register as a sole proprietor you just need to register with Department of Trade and Industry (DTI) through BNRS. Just answer the fields and in a matter of minutes you will have your e-certificate as proof of your registration. So it is fast and easy!

If you choose to establish a Corporation, this is a bit complex process and not as fast compared to sole. You need to draft the Articles of Incorporation, By Laws and Treasurer’s Certificate. Know how much would be your Authorized, Subscribed and Paid up Capital will be send it to the Securities and Exchange Commission for review and wait til gets its releaseed about 2-3 weeks sometimes a month or two pa nga.(so if you have zero knowledge best you outsource this to a lawyer or an accountant) .

(Will be coming out with a step by step process of registration with DTI and SEC sooooooon!)

As to the liability against debtors

When you register as a SOLE PROPRIETOR you have a GENERAL LIABILITY.

What does GENERAL LIABILITY mean?

This means when your business go under (pag nalugi) and you have outstanding debts(may utang ka pa sa business) your creditors (pinag kaka utangan mo) may get all of your assets as in all assets EVEN YOUR PERSONAL ASSETS in order to settle your debts even if that debt is because of your BUSINESS.

In short gang sa SOFA at PLASMA TV mo kung kina-kailangan ay pwedeng hatakin ng pinagkakautanagan mo be it suppliers, banks, employees and taxes.

How bout when you choose to register as a CORPORATION?

When you register as a CORPORATION your liability is LIMITED!

What does LIMITED LIABILITY mean?

It means when your business goes under and you decide to close your corporation and you still have outstanding debts. Unlike the sole props, the debtors can only run after the ASSETS OF THE BUSINESS only! (oo safe yung sofa at plasma tv mo).

Why is this so?

Because a corporation is treated a separate and distinct entity from the owners in the eyes of the law. This called corporate fiction and their only limited times that the corporation fiction can be pierced but generally it can’t be (will discuss this in a separate blog)

As to taxes (income taxes to be exact).

If you decide to be register as sole proprietor what will be your tax implication?

Well for income tax purposes. Individuals maybe at a maximum of 35%!

How bout for corporations?

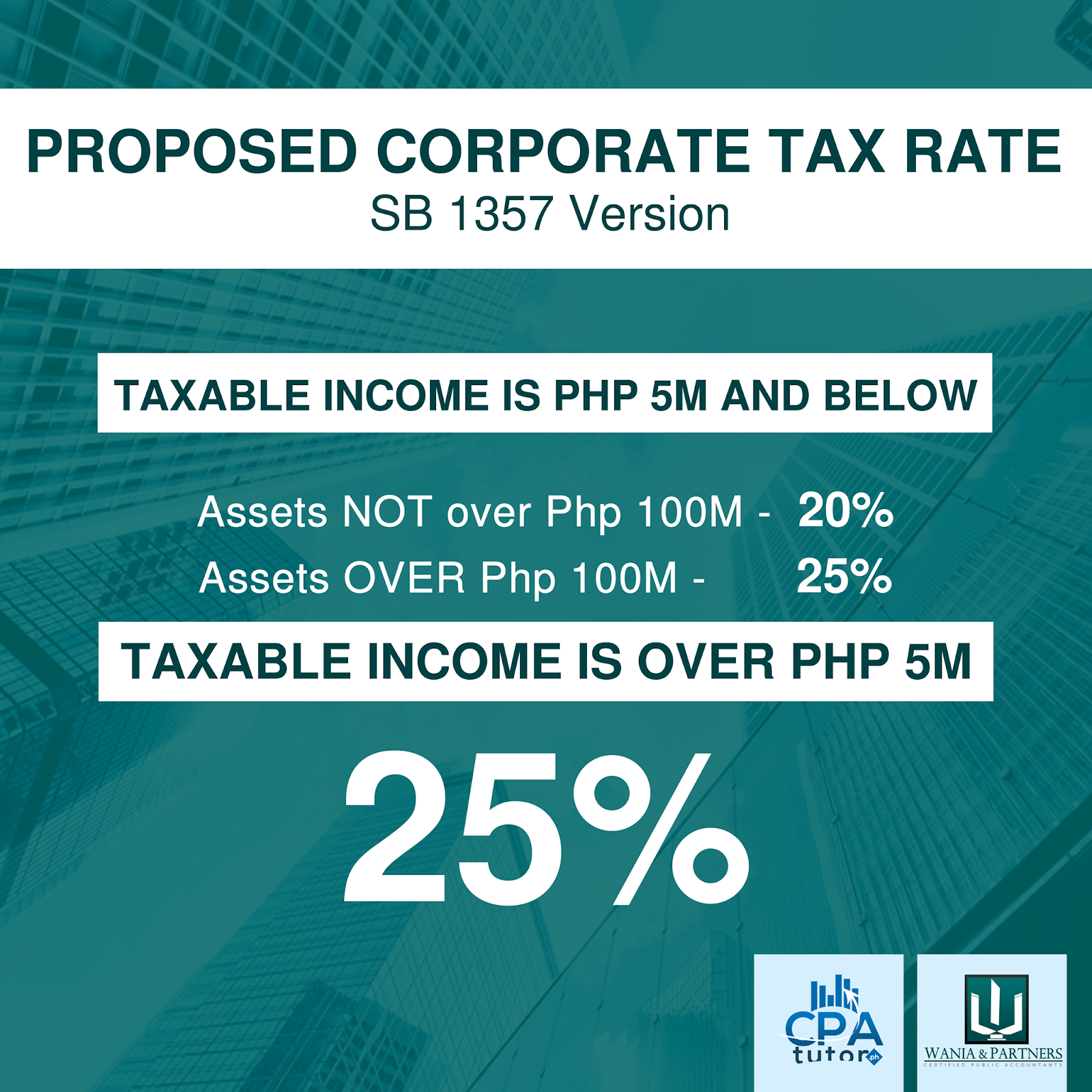

Corporations are taxed on its taxable income at 30% for now(hopeful for the tax reform to be signed where the tax rate may go down as 20%!… read : Ano bang bago dito? CREATE BILL?)

As to the number of owners (of course)

Ordinarily, if you are the only ONE the sole who will own and manage the business sole proprietorship is for you. The business papers will be under your name that includes your DTI, BIR and Business Permit will be named under the sole owner.

If you have two to five (or even as high as fifteen) who will own and/or manage the business then it is best to put up CORPORATION. The business papers especially the Articles of Incorporation will clearly lay out the names of the stockholders of the incorporators (the first company stockholders) and the amount of shares they bought which will determine their percentage of owners of the company and the amount of dividends (share on/ the net profit).

Recap

Registration : Mas madali at mabilis pag sole prop

Liability:Mas protektado ang personal assets mo pag CORPO

Tax (Income Tax) : Mas mababa ang tax pag CORPO at maaring mas bumaba pa

So after reading this difference you might think na mas ok pala mag corporation. However pano pag mag isa lang talaga ako?

But did you know you can register as a corporation even if you are just only one? How?

This is through establishing a ONE PERSON CORPORATION which is now allowed by virtue of the REVISED CORPORATION CODE.

Want to know how to establish your own ONE PERSON CORPORATION. Sign up in our seminar in partnership with Attorney Nico B. Valderama, CPA, MPM

Sign up here: Join the seminar!

We would love to hear from you feel free to comment what you have learned or what topics would you like us to feature. Will be coming out with the part 2 of this article next week!